Zakat & Business

Many questions that American Muslims have about zakat are related to wealth that is acquired through business and investment, debt and liquid assets.

Many questions that American Muslims have about zakat are related to wealth that is acquired through business and investment, debt and liquid assets.

According to Shaykh Qardawi, if the contributor has access to the fund and can spend it at will, then zakat is due every year on the fund, like someone who pays zakat on loans made to others that are expected to be paid back. However, if one has no access to the fund, then zakat is to be given only when the money is received, that is, at the time of retirement.

Opinions differ. Some hold it to be under the control of an independent agency and others under the employee’s control (minus penalties). It may also be deemed a “good” loan, which is to say a debt likely payable in the future.

The individual should consider all such accounts—401(k), Keogh, IRA, SEP-IRA, Roth IRA, etc.—as part of personal net worth because the employee has eventual access to and ultimate control over the funds. As a type of savings, it is zakatable at the rate of 2.5 percent annually (Zakat Calculation, 50-52). Usually not all the money is accessible to the investor for withdrawal, up to 50 percent normally being allowed. The following formula by Dr. Salah Al-Sawy, secretary general for the Assembly of Muslim Jurists in America (AMJA), may be helpful: (WA)-(PP)-(PT)=(ZA).

Withdrawal Amount - Prescribed Penalty - Prescribed Tax = Zakatable Amount

Yes. Two major opinions regarding zakat on such assets concur that stocks, shares, and bonds are zakatable.

This opinion holds that shares and bonds are analogous to commodities purchased for resale like any other business good. Therefore, their zakat is calculated at a standard personal wealth rate of 2.5 percent of total portfolio value at the zakat due date because they are bought with expectation of profit, and readily traded for money. Here stocks and bonds are both treated as liquid assets regardless of the economic activity of the issuing corporation. This is the opinion of Shaykhs Abu Zahra and Khallaf. Shaykh Qardawi believes that both opinions are sound and suggests that either method can be selected by the zakat administration or payer.

Note: If the company pays zakat on all shares, the shareholder does not pay zakat because there is no double payment of zakat.

Zakat Foundation of America endorses the opinion that stocks and shares are trading goods, zakatable at 2.5 percent. The form recommends individual shareholders as the zakat payers.

Confusion may arise in assessing zakat on stocks for short-term traders. Recall that the passage of a year is required on nisab only, not all of one’s zakatable earnings. So, short-term traders should estimate stock values on an established annual zakat due date, regardless of stock purchase dates or value fluctuations, and pay 2.5 percent of total portfolio value.

Such wealth is considered analogous to “produce of plowed land,” and therefore its zakatable portion accrues at a rate of 10 percent of the return. If the owner purchased these instruments with the intention of long-term investment, it is the actual gain, not the productive capital itself, that is zakatable.

So shares of corporations are zakatable at 10 percent on the dividends of these shares. This view also distinguishes between shares and bonds. Bonds are analogous to debts that one can expect to be paid. Zakat, therefore, is payable on them every year at a rate of 2.5 percent. Modern Muslim scholars concur upon this ruling.

Most Islamic jurists also agree that consideration of the market value of your portfolio is allowable from the beginning to the end of the solar Gregorian calendar year for ease of calculation purposes, but 10.3 percent of the gain should be paid to offset the difference between the lunar Hijri and solar Gregorian calendars.

Zakat is due only upon lawful money. Islam considers interest unlawful, and bonds that earn interest are no exception. Bonds are nonetheless capital and, therefore, zakatable. The prohibition on accepting interest does not exempt the recipient from paying zakat on the principle price for which the bonds were originally purchased. Zakat is not calculated on the interest income of the bonds. Rather, all interest income is to be given to the poor (separately from zakat) with no expectation of divine reward. (Fiqh az-Zakat, 331-338).

Scholars generally classify debt as “good” and “bad,” similar to current fiscal credit categories.

A good debt is acknowledged by the debtor, who expresses a willingness to pay. Lenders must pay zakat on good debt every zakat-year (hawl).

A bad or delinquent debt will likely not be repaid, either because the debtor is insolvent or he denies a debt for which there is no corroborating proof. The lender does not pay zakat on delinquent debt, according to the majority of scholars. But should the lender ever receive repayment on a past bad debt, he is to pay the zakat due on it for one year only (Fiqh az-Zakat, 74-76).

Opinions differ. The Malikis, Hanbalis, and Hanafis hold that debt reduces the zakatable wealth of the debtor by the amount of the outstanding debt. Accordingly, debts are deductible from assets subject to zakat (Fiqh az-Zakat, 90-94).

Shafi’is argue that zakat is wealth under the payer’s control. Therefore, if one has nisab for a zakat-year one still pays zakat on the zakatable wealth in one’s possession even if one’s debts, were they to be deducted or paid, would consume one’s wealth entirely. That is, one pays zakat on one’s eligible wealth, unless one chooses to pay debts before estimating zakat dues.

This position concurs with the statement of ‘Uthman ibn ‘Affan, third Caliph of Islam, who said in a Friday address (khutbah): “This is the month of your zakat. Whoever among you owes debts, pay them back, that you may commence paying the zakat on your assets” (Al-Amwal, 437). In another version reported by Malik, ‘Uthman reportedly said: “Let one in debt repay his debt, then pay zakat on his remaining assets.” (Al-Talkhis, 178) This address came from the pulpit in the presence of many Companions. None objected.

Optimally, if debts come due (or are payable) on or before the zakat due date, one should repay them and then pay zakat on all remaining zakatable wealth. Some scholars disallow debt deduction if debt due dates come after the zakat due date.

Zakat is the right of the poor and eligible. It is unjust to incur large debts in extravagance and then invoke debt deductions at the time of calculating zakat. This, in effect, denies the destitute their basic needs and rights for the sake of one’s extravagant lifestyle. If all one’s zakatable wealth is paid on without resorting to debt deduction, it will usually not cause a great increase in one’s zakat payment (Zakat Calculation, 33-34).

Being in business might involve investing money in the purchase or rent of property, furniture, and equipment. It may also involve having goods to sell. Another factor is the income generated from the business, which may be reinvested in the business or distributed to owners. Scholars classify business assets into two categories for the purpose of zakat calculation: Liquid assets that can be converted readily to cash, and fixed assets that are used to produce revenue but will not be converted to cash for more than a year.

Liquid assets are goods such as business inventory that can and will be readily converted to cash. They include anything purchased with an intention (or openness) to sell or trade for profit, including land and lots, houses, buildings, furniture, clothing, foodstuff, machinery, jewelry or any salable goods. Thus, even livestock for resale fall in this category (although the amount required for nisâb differ).

Zakat for a business is calculated on the zakat due date (or estimated prior to that date) according to the following formula:

Appraised Merchandise Wholesale Value (A) plus Cash on Hand and in Deposit (C) plus Good Debt Owed to Business (GD) minus Eligible Debt* times .025 equals Zakat Payment

((A+C+GD) -(ED)) x 2.5 percent = Zakat Due

*Subtract eligible debts if you follow a juristic school (madhhab) that permits debt deduction. If the balance reaches nisab (the monetary equivalent of 85 grams of pure gold), then zakat is 2.5 percent of the balance. (Fiqh az-Zakat, 203, 213-216).

GENERAL RULE: Zakat is calculated based on the market value of an asset and distributed immediately upon the due date.

For example, one determines the market value of gold, a stock portfolio, liquid assets, or luxury items in excess of personal use (i.e. jewelry, art, collections, etc.) as of the zakat due date. If one delays calculating zakat on shares whose prices fall or rise, zakat is still paid on the market value as of the due date (Zakat Calculation, 30-31). Commercial commodity values are their wholesale price on the zakat due date, whether they are designated retail or wholesale and whether they are higher or lower than the retail price. This is a majority opinion.

Zakat is assessed for rental property on growth only. The fixed asset itself is exempted from zakat , which is calculated at 2.5 percent of net income after all expenses are deducted for the zakat year.

Fixed assets are not themselves income generating but help other assets generate income or produce. So store fixtures, computers, tables, even buildings or machinery that are not generating income but merely housing or running one’s business are all zakat-exempt.

Exploited assets are possessions obtained, not for resale, but to generate income and to provide benefit to their owners. These include assets rented for profit, such as residential buildings, means of transportation, and anything rented out for profit.

Rental businesses (equipment, cars, etc.) pay zakat on (1) the wholesale value of all rental assets (considered trading goods) at 2.5 percent; and (2) on net income at 2.5 percent (There is an alternative calculation method (see answers pp. 54-56) (Zakat Calculation, 49-50).

Agricultural produce is zakatable. Zakat is due on everything land produces that can be eaten and stored (such as grains, beans, fruit, dates, etc.) Nisab on crops is measured in five volume units individually called wasq (1 wasq = 130.56 kg of wheat). Five wasqs equal 653 kilograms. This is the nisab on agricultural yields.

There are two agricultural types of product: (1) At cost, and (2) without cost. The zakat rate changes accordingly (Fiqh az-Zakat, 228-229, 242):

Output from Irrigated Land: Zakat rate is 5 percent of net value of harvest—after deduction of costs, including irrigation, fertilizer, and operating expenses

Output from Unirrigated Land: Zakat rate is 10 percent of gross value of harvest, since land is being watered mostly by rain, natural springs (There are straight mathematical percentage changes if land is partially irrigated for half the time, a third of the time, a quarter of the time, etc.).

No. There is no zakat on land value, only on value generated (i.e., the harvest). If land is leased to a farmer, the farmer pays zakat on the crops, the owner on the rent received. Zakat is 2.5 percent of net rental income for the landowner (see answers pp. 51-55 for alternative calculations (Fiqh az-Zakat, 255-256; Zakat Calculation, 27).

Yes. Livestock is zakatable. Domestic animals and poultry for personal use are not zakatable (including for food, use, and enjoyment). Working animals for cultivation, etc. are zakat-exempt. Nisab and zakat rates on various animals follow (Fiqh az-Zakat, 104-105, 131-137).

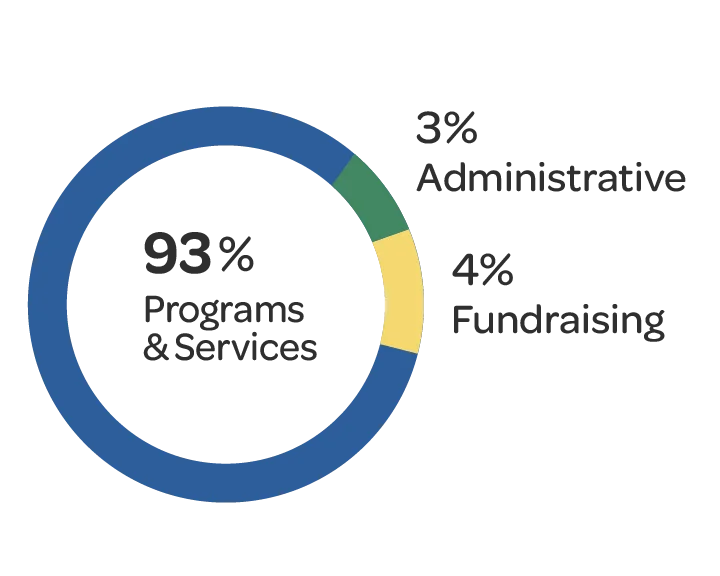

In 2025, 93¢ from each dollar donated went directly toward programs serving those in need, 3¢ went to administrative costs & 4¢ went to fundraising costs