Zakat Assessment

In order to accurately calculate your zakat, it is important to know what types of wealth zakat is due on and what types of wealth are non-zakatable.

In order to accurately calculate your zakat, it is important to know what types of wealth zakat is due on and what types of wealth are non-zakatable.

Zakat is payable on five types of material wealth:

Personal wealth and assets

Liquid and exploited assets

Agricultural produce

Livestock

Treasure

Also, there are three major conditions for zakat on these types of wealth:

Sole, exclusive ownership

Growth (actual or potential)

Passage of a zakat-year

See the Zakat Calculator.

Yes. These are called “exploited assets” and are considered a form of business wealth. While liquid assets may be sold, exploited assets remain with the owner as permanent capital. They are possessions obtained for the purpose of generating income and to benefit their owner.

Exploited assets include anything rented out for profit, such as residential buildings, equipment or means of transportation. They also include producer animals such as sheep for wool, cows for milk, or bees for honey.

Liquid assets are goods that can be easily sold, usually for a profit. They are zakatable only once in the zakat-year and fit all the other conditions of zakat of any other zakatable wealth.

No. A fixed asset is one that on its own is not income generating, but helps other assets generate income. Store fixtures, computers, tables, even buildings or machinery that are not generating income but merely housing or running one’s business are all zakat-exempt. The test for whether an asset is fixed or exploited is whether the asset is generating profit in and of itself. A non-income generating building is a fixed asset (non-zakatable) but a hotel is an exploited asset (zakatable on its net income).

On the growth of an exploited asset, zakat is assessed after deductions (taxes, wages, debt, maintenance, etc.) based on its appraised value plus the income it generates (figuring in loans to others) and then paid at the rate of 2.5 percent. This means that the passage of a zakat-year does not apply on individual payments received through rent or on income earned. It means that the net earning and value of the asset—even a rental fee that comes in the day before the zakat-year ends—is calculated and paid on the zakat due date.

Yes. The opinion is somewhat involved, but it can be summarized as follows. Some modern fiqh luminaries (including Shaykh Yusuf Qardawi from our own time) endorse analogizing the zakat of exploited assets to agricultural land (with some modifications). But they also add to this the fixed assets of industrial equipment, plants and machinery, on the grounds that they are not tools of a craftsman, but productive and growing capital (see Fiqh az-Zakât, 304). Shaykh Yusuf makes a further distinction between these productive assets by categorizing them as “fixed” (the industrial plants, etc.) or mobile (like vehicles or honey producing bees).

The analogy with agriculture is that the land is zakat exempt, but the product of the land (i.e., the crop) is zakatable at the rate of 10 percent of the net harvest value, if naturally watered, and five percent of the harvest profit, if irrigated. So Shaykh Yusuf likens productive exploited assets that are fixed, and fixed industrial assets to the non-irrigated crop zakat rate (10 percent) “when it is possible to know the net income after deducting costs, as is the case in business corporations.”

But if it is difficult to determine net income, then zakat is calculated at the rate of five percent of the profit (see Fiqh az-Zakât, 305-06) for the exploited assets that are fixed, and fixed industrial assets.

No. A hawl, or zakat-year, only has to pass on the nisâb of productive assets in BOTH opinions, which agree that the hawl need NOT elapse over all the wealth before it is zakatable. This is, of course, true for crops, which are due upon harvest, for obvious reasons.

With (productive) fixed and exploited assets—just like with personal wealth—zakat is paid on all net income for the zakat-year. It is paid on the zakat due date for everything that remains with one after basic living expenses for oneself and one’s dependents have been paid out for that year. So a hawl does not have to elapse on each dollar received.

GENERAL RULE: Zakat is potentially due on all products whose sources are not zakatable.

All types of growth yields are zakatable, whether or not their origin is subject to zakat—like crops from land, honey from bees, dairy from livestock, eggs from poultry, silk from silk-worms, and so forth. The producers (bees, livestock, poultry, etc.) are themselves zakat-exempt (unless one is actually breeding the producers for sale or using the producers themselves as trade assets, in which case their zakat is assessed as a liquid asset). Zakat rates vary for different types of wealth, such as money, agricultural products, livestock, and natural resources. Shaykh Yusuf Qardawi assesses the zakat rate on such yields as 10 percent of net income. Those jurists who consider non-pasturing producers as trade assets assess the zakat rate at 2.5 percent on both principal and growth (Fiqh az-Zakât, 274).

The most common zakatable wealth is cash on hand and in banks, stocks, and retirement and savings funds. The amount of zakat due on this wealth is 2.5 percent of its combined total value as of the annual zakat due date.

Yes. Earned income is the primary category of personal wealth today. It includes salaries and professional fees that result from labor and specialized tasks. Whatever of it is spent on personal and family expenses prior to the end of the zakat-year is not subject to zakat. But whatever is left of one’s earned income at the end of the zakat-year is subject to zakat— whether or not a full zakat-year has elapsed over the portion in hand. On the date the zakat falls due, whatever portion of the earned income is in hand, even if it is a check received that day, within the zakat-year, zakat must be paid on it if the total yearly salary and/or fees exceed the nisâb, the monetary equivalent of 3 US OZ. of pure gold. Salaries and fees received through the year are tabulated cumulatively.

Many modern Muslim jurists and scholars consider net earned income to be zakatable, including ‘Abd Al-Rahmân Hasan, Muhammad Abû Zahrâ, ‘Abd Al-Wahhâb Khallâf, Muhammad Al-Ghazali, Monzer Kahf, and Mahmûd Abû Sa’ûd (Kahf, The Calculation of Zakah, 5; Abû Sa’ûd. About the Fiqh of Zakât, 20).

The zakatable amount is the residual money left over from earnings at the end of one fiscal year. This does not mean zakat is due on the flow of income itself during the year. It is applied to whatever remains of one’s annual income at the end of the year (i.e., after taxes and expenses, and in all its forms and places of deposit collectively). (Fiqh az-Zakât, 310, 325)

According to the majority of schools, Mâlikî, Shâfi’î, and Hanbalî, there is no zakat on women’s jewelry, whether of gold, silver, diamonds, pearls, minerals, or precious stones, so long as they are for personal use, not sale or rental.

The Hanafî position is that jewelry is zakatable.

If such jewelry attains a quantity of extravagance or is used as a store of wealth, then the surplus is zakatable (Fiqh az-Zakât, 184, 186-188, 192, 199).

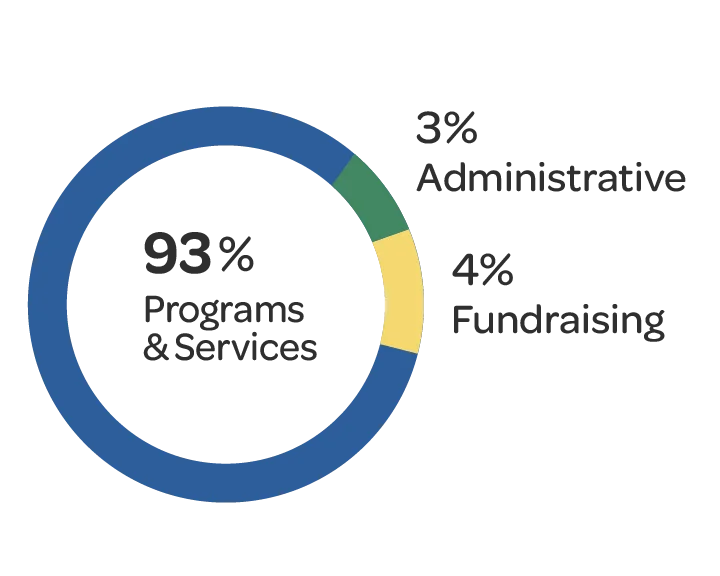

In 2025, 93¢ from each dollar donated went directly toward programs serving those in need, 3¢ went to administrative costs & 4¢ went to fundraising costs